You may consider a conventional loan if your DTI is too high and you are worried about the high interest rate. This type is convenient because it can be obtained with as little down as 3%. This type of loan comes with its risks. Before applying to a conventional loan, it is necessary to reduce your DTI.

Preparing to apply for a conventional mortgage

You should apply for a conventional loan if you need funding for your business. Although these loans are quick and easy to get, they do require high credit scores and other financial qualifications. There are other loan options available for those with less-than-perfect credit. There are many options available for you, including low interest rates and low fees as well as flexible repayment options.

You should organize your finances before you apply for a conventional mortgage. Make sure that you pay off any debts you have, increase your income, and save for a down payment. Follow these guidelines to increase your chances for approval and secure the funding you require.

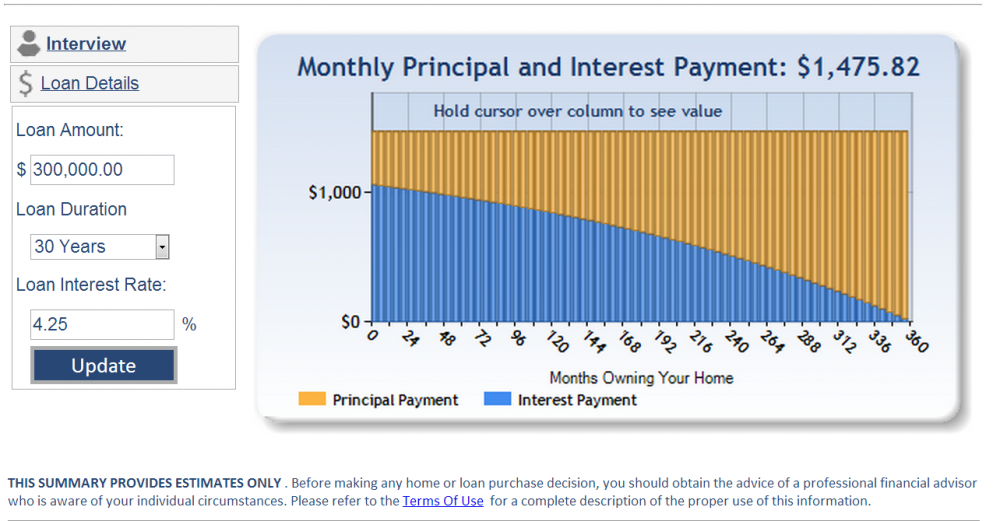

A conventional loan is available with as little 3% down

A conventional loan for as little as 3.3% down is a good option for many homebuyers. This type of loan will be most affordable if you have excellent credit. In addition, it requires only a small down payment, so you can save your liquid reserves for other expenses related to your new home.

These loans come in two forms. The first is the 3% down loan from Fannie Mae, which is intended for first-time homebuyers. In order to qualify for this type of loan, you must not have owned a home for at least three years. You can also apply for a federally insured loan that is 3% less.

Convenience and ease of a conventional loan

Conventional loans are the most common type. They can be used in a number of ways. They are easier to get approved for, have fewer restrictions, can be used for virtually any property and can cover nearly all types of property. A conventional loan is also available without mortgage insurance. It has a lower interest rate and no need for mortgage insurance.

A conventional loan is not insured by the federal Government, but it is still popular among borrowers who have excellent credit, stable income and enough money to pay down the mortgage. It is also a good option for those with less-than-perfect credit or first-time homebuyers.

There are risks of defaulting on a conventional mortgage

Conventional loans can be cheaper than government-backed mortgages but they come with their own risks. Lenders who issue these loans do not have federal protection, and can lose a lot of their money if the borrower defaults. These loans can be harder to obtain than government-backed Mortgages.

Conventional loans can be classified into one of two types: conforming or non-conforming. Conforming loans refer to those that comply with lending standards set forth Fannie Mae & Freddie Mac. Non-conforming loans exceed conforming loan limits. Typically, a non-conforming loan will come with higher interest rates, stricter underwriting requirements, and higher down payments.

FAQ

Do I need flood insurance

Flood Insurance covers flooding-related damages. Flood insurance protects your belongings and helps you to pay your mortgage. Find out more information on flood insurance.

How many times may I refinance my home mortgage?

This is dependent on whether the mortgage broker or another lender you use to refinance. You can typically refinance once every five year in either case.

Is it possible to sell a house fast?

You may be able to sell your house quickly if you intend to move out of the current residence in the next few weeks. There are some things to remember before you do this. First, you will need to find a buyer. Second, you will need to negotiate a deal. The second step is to prepare your house for selling. Third, you must advertise your property. Finally, you need to accept offers made to you.

What's the time frame to get a loan approved?

It all depends on your credit score, income level, and type of loan. It usually takes between 30 and 60 days to get approved for a mortgage.

How do I know if my house is worth selling?

If your asking price is too low, it may be because you aren't pricing your home correctly. Your asking price should be well below the market value to ensure that there is enough interest in your property. For more information on current market conditions, download our Home Value Report.

What is a "reverse mortgage"?

A reverse mortgage allows you to borrow money from your house without having to sell any of the equity. It allows you to borrow money from your home while still living in it. There are two types available: FHA (government-insured) and conventional. You must repay the amount borrowed and pay an origination fee for a conventional reverse loan. FHA insurance covers repayments.

How do I repair my roof

Roofs may leak from improper maintenance, age, and weather. Repairs and replacements of minor nature can be made by roofing contractors. Contact us for further information.

Statistics

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

External Links

How To

How to become an agent in real estate

Attending an introductory course is the first step to becoming a real-estate agent.

Next, you will need to pass a qualifying exam which tests your knowledge about the subject. This requires that you study for at most 2 hours per days over 3 months.

Once this is complete, you are ready to take the final exam. For you to be eligible as a real-estate agent, you need to score at least 80 percent.

If you pass all these exams, then you are now qualified to start working as a real estate agent!