It is crucial to conduct thorough research before signing a deal to purchase a pre-foreclosure property. This can be done in several ways. The first step is to find out why the property was pre-foreclosed. The second is a physical inspection. The third step is the due diligence of legal documents and down payments. You can apply for loans from hard-money lenders if you don't have the money to cover the down payment. You should also know the total amount of expenses that you have incurred over the past year.

Option to stop pre-foreclosure

Although the foreclosure process can be difficult, there are ways to stop it. You can negotiate with your lender to modify your loan. This will allow you to pay less over a longer time period. After you agree to a loan modification you can stop foreclosure proceedings and avoid the need to sell your house. Your lender might try to sell your home to get the remaining balance.

Filing for bankruptcy is another option to stop pre-foreclosures. In most cases, filing for bankruptcy will declare you insolvent and stop the foreclosure process. Your lender may be able to offer loan modifications if bankruptcy is not an option.

Steps to be taken during the process

If you're in the pre foreclosure process, you should be aware of your options. Pre-foreclosure is avoidable if you pay your debts early. You will most likely be able buy pre-foreclosure property for a fraction of the amount you owe to your lender. However, it is important to do your research before making any purchase. Due diligence includes all aspects of purchasing a preforeclosed property, including the legal, financial and physical. Financial due diligence also includes reviewing the down payment and mortgage payments made on your property. Also, you should have your income and expenses from the last year verified.

Another option is to sell your pre-foreclosure property. This option avoids the entire foreclosure process and saves the bank both time and money. However, it's still risky since it could fall through before the pre-foreclosure sale is completed. You risk losing your deposit if the sale doesn't go through. Also, the seller may have the right to refuse your offer or cancel the transaction.

Common lenders involved

Pre foreclosure is a process that involves two types of lenders. There are two types of lenders involved in pre foreclosure: conventional lenders and hard money lenders. A hard money lender will pay cash to purchase a property which has fallen into default. They are less concerned about the credit score of borrowers and more interested in the property's financial viability. A property's after-repair price determines its profitability.

These investors can purchase properties that are in foreclosure for less money than their lender owes. However, they should note that conventional lenders are unlikely to approve these loans. They should instead try to get a loan from a hard money lender. If this fails, they should seek out a loan with another hard money lender.

You should not panic if you're facing pre-foreclosure. Keep an eye on credit reports. You should keep in touch with your lender to ensure that you are informed about any potential changes. It's important to take action so that foreclosure does not occur.

FAQ

What's the time frame to get a loan approved?

It depends on several factors such as credit score, income level, type of loan, etc. It usually takes between 30 and 60 days to get approved for a mortgage.

Is it better for me to rent or buy?

Renting is generally cheaper than buying a home. However, you should understand that rent is more affordable than buying a house. You also have the advantage of owning a home. You will be able to have greater control over your life.

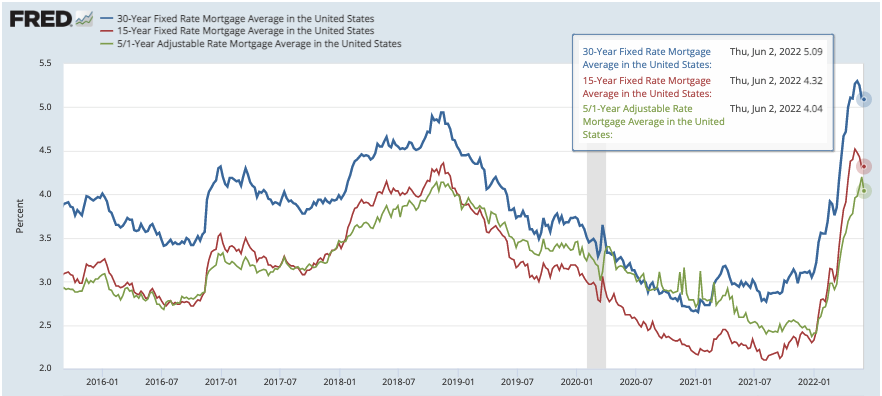

How do you calculate your interest rate?

Market conditions can affect how interest rates change each day. The average interest rate for the past week was 4.39%. Multiply the length of the loan by the interest rate to calculate the interest rate. For example, if you finance $200,000 over 20 years at 5% per year, your interest rate is 0.05 x 20 1%, which equals ten basis points.

Statistics

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

External Links

How To

How to be a real-estate broker

You must first take an introductory course to become a licensed real estate agent.

Next, you will need to pass a qualifying exam which tests your knowledge about the subject. This involves studying for at least 2 hours per day over a period of 3 months.

Once this is complete, you are ready to take the final exam. To be a licensed real estate agent, you must achieve a minimum score of 80%.

These exams are passed and you can now work as an agent in real estate.