This article will explain how to calculate PMI for tax purposes. PMI is a type or mortgage insurance that can be deducted from your tax. The percentage of your total loan will determine the amount you'll pay. The loan amount you borrow will affect how much you pay. When the loan balance is 78%, the mortgage insurance must be terminated. This happens usually around the age of 12 years.

Private mortgage insurance that is tax-deductible

Tax-deductible private mortgage insurance is a type of mortgage insurance that is paid by the borrower. This type of insurance is affordable and plays a crucial role in the mortgage finance process. PrivateMI protects homeowners from financial loss by helping to lower mortgage payments. With rising interest rates and a slowing housing market, homeowners are paying more monthly for home loans. Additionally, the expense is tax-deductible and can be cancelled if there is enough equity in the home.

Federal authorities extended the mortgage insurance premium deduction to borrowers through 2020. It is important to remember that the deduction applies only to private mortgage premiums. It is not available for cash out refinances or home equity loan. A borrower must include their income and itemize taxes to be eligible for the deduction. On mortgages that have been in place for three years or more, the borrower pays mortgage insurance premiums.

LTV

A few points to remember if you are curious about how PMI calculates. First, the amount of PMI that you are required to pay is determined by your loan-to–value ratio, also known as LTV. LTV is the amount of the loan divided by the total amount of the home's value. The lender might deny your request if this ratio is too high. The lender may request a broker price opinion (BPO) from the broker to confirm the market value of your home and calculate the LTV. You can also request to end your PMI payments early. BPOs or appraisals are usually performed at your expense. However you could save hundreds of money if your mortgage insurance is terminated early.

Your down payment is also a factor in determining the LTV. Typically, a down payment of 10% will equal a 90% LTV ratio. In order to avoid PMI, you'll need to make a minimum of 80% down payment if you have 10%. If your mortgage payment exceeds 80% of the purchase price, PMI will be required until you reach 15 years.

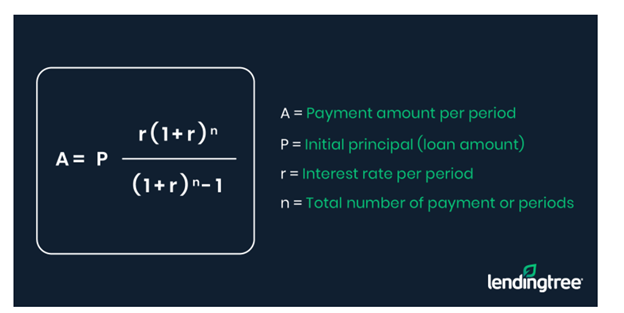

Calculating the PMI

The data from soil chemistry can be used for the calculation of the PMI. Such analysis can help in medical-legal cases as well as in humanitarian recovery. The confidence intervals are critical to the accuracy of the results. They should not exceed 95% of the nominal value. In order to determine the accuracy of the calculation, there are several important factors to consider, such as the cause of death, coverage proportion, and confidence interval.

PMI is a form of additional insurance. This is necessary for borrowers who don’t have sufficient funds in order to fully pay off the loan. This additional insurance, depending on the loan-to value ratio, can lower the risk of some mortgages.

Getting out of paying PMI

There are several ways you can avoid paying PMI for a mortgage. One way is to reduce the loan-to-value ratio to less than 80 percent. To do this, you must make regular payments on your mortgage and prove you don't have any other liens. Information about how to cancel PMI is also available in the Homeowners Protection Act.

You can also pay at least 20% down. This will allow you to avoid PMI over a longer time. Some of these methods are simpler than others. However, it may take some time to complete them all.

FAQ

How can I find out if my house sells for a fair price?

Your home may not be priced correctly if your asking price is too low. You may not get enough interest in the home if your asking price is lower than the market value. To learn more about current market conditions, you can download our free Home Value Report.

What should I look for in a mortgage broker?

People who aren't eligible for traditional mortgages can be helped by a mortgage broker. They compare deals from different lenders in order to find the best deal for their clients. Some brokers charge a fee for this service. Other brokers offer no-cost services.

Can I afford a downpayment to buy a house?

Yes! Yes. These programs include government-backed loans (FHA), VA loans, USDA loans, and conventional mortgages. More information is available on our website.

Is it possible for a house to be sold quickly?

It might be possible to sell your house quickly, if your goal is to move out within the next few month. Before you sell your house, however, there are a few things that you should remember. First, find a buyer for your house and then negotiate a contract. Second, prepare your property for sale. Third, it is important to market your property. Lastly, you must accept any offers you receive.

Statistics

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

External Links

How To

How to find houses to rent

For people looking to move, finding houses to rent is a common task. It can be difficult to find the right home. When you are looking for a home, many factors will affect your decision-making process. These include location, size, number of rooms, amenities, price range, etc.

We recommend you begin looking for properties as soon as possible to ensure you get the best deal. For recommendations, you can also ask family members, landlords and real estate agents as well as property managers. This will allow you to have many choices.