FHA loans are a popular choice for first-time homebuyers. They have less stringent approval requirements. FHA loans are less expensive than conventional loans, which require 6% down and 3.5% down. There are also no income verification or home appraisal requirements. FHA streamline is also a great option because you can get an FHA Loan even if you have another home. However, you cannot refinance the old home into a new mortgage, unless you are refinancing it as an investment property. Also, the new mortgage can't be an adjustable rate mortgage (ARM), nor a cash-out refinance.

Limits to multiple FHA loans

There are strict limits to how many FHA loans one borrower can get at once. Borrowers are limited to one FHA loan at a given time. The first must be paid off before they can apply for the second. There are exceptions to the rule. It is possible for a borrower with certain circumstances to get two FHA loans.

The limits for an FHA loan are determined by the Federal Housing Administration (HUD). The number of units and location of the property determine how much money you can borrow. For homes with multiple units, the limits are higher.

Minimum down payment

FHA loans can only be obtained if you have at least 10 percent down on the purchase price. You can also get assistance from the state and government for your down payment if money is tight. As part of your downpayment, you can also get a gift from family or friends. The FHA will not approve any loan that requires borrowing to pay down the down payment.

You must also meet income and credit requirements. To qualify for an FHA Loan, you must also show proof of your identity as well as assets. You must also have at least a 500 credit score to qualify. Low credit scores can lead to higher interest rates, so make sure you pay close attention to your score.

For an FHA loan you will need to meet the following requirements

An FHA loan application requires you to show proof that you can afford your monthly payments. To prove your income, you will need to provide proof such as bank statements, pay stubs and tax returns. It is important to have sufficient funds to cover the closing costs and down payment of your new home.

When applying for a loan, it is important to take into account the minimum debt-to income ratio (DTI). The FHA requires borrowers to maintain a DTI of under 43%. However, some lenders may accept applicants with higher DTI ratios. Also, your credit score will play an important role in determining your loan eligibility.

Requirements to qualify for an FHA loan after a waiting period

FHA loans are not easy to get a mortgage for people who have low credit ratings or don't have enough money down. The interest rates on FHA loans are generally lower than those for conventional mortgages, as they are guaranteed by the government. FHA lenders don’t have to pay risk-based insurance for mortgages. This means that even borrowers who have poor credit ratings will be approved with a higher chance.

A home loan is a mortgage that you apply for after your house has been sold. There are some requirements you need to fulfill in order to get an FHA loan after a foreclosure. The main criteria include a reduced income of 20% or less, a credit report showing positive changes, and a down payment of 20% or more. The rules regarding extenuating circumstance are important as they can help you qualify for an FHA loan.

There are several ways you can qualify for an FHA Loan after the waiting period

After completing the waiting period, there are many ways you can qualify for an FHA loan. One way is to show lenders that you have recovered your credit and made twelve months of mortgage payments before your waiting period began. For an FHA loan you need a credit score of at least 580. If you have had a foreclosure or any other credit-related event in the past, some lenders may require a higher score.

Some lenders will allow borrowers who have been declared bankrupt to apply for exceptions. One reason for filing bankruptcy is financial hardship. Filing for bankruptcy is a big derogatory mark on a credit report, so many people who file for bankruptcy end up giving up on home ownership. If you are able to prove financial recovery, you may be eligible for an FHA loan.

FAQ

What should you think about when investing in real property?

The first step is to make sure you have enough money to buy real estate. If you don't have any money saved up for this purpose, you need to borrow from a bank or other financial institution. Aside from making sure that you aren't in debt, it is also important to know that defaulting on a loan will result in you not being able to repay the amount you borrowed.

You must also be clear about how much you have to spend on your investment property each monthly. This amount must be sufficient to cover all expenses, including mortgage payments and insurance.

Also, make sure that you have a safe area to invest in property. It would be best to look at properties while you are away.

What are the benefits of a fixed-rate mortgage?

With a fixed-rate mortgage, you lock in the interest rate for the life of the loan. This ensures that you don't have to worry if interest rates rise. Fixed-rate loans also come with lower payments because they're locked in for a set term.

Is it possible fast to sell your house?

If you plan to move out of your current residence within the next few months, it may be possible to sell your house quickly. You should be aware of some things before you make this move. First, you need to find a buyer and negotiate a contract. You must prepare your home for sale. Third, you need to advertise your property. Finally, you should accept any offers made to your property.

How much does it cost to replace windows?

Windows replacement can be as expensive as $1,500-$3,000 each. The cost to replace all your windows depends on their size, style and brand.

What are the chances of me getting a second mortgage.

Yes. But it's wise to talk to a professional before making a decision about whether or not you want one. A second mortgage is usually used to consolidate existing debts and to finance home improvements.

What are the top three factors in buying a home?

Location, price and size are the three most important aspects to consider when purchasing any type of home. Location is the location you choose to live. Price refers to what you're willing to pay for the property. Size is the amount of space you require.

What amount should I save to buy a house?

It depends on how much time you intend to stay there. Start saving now if your goal is to remain there for at least five more years. However, if you're planning on moving within two years, you don’t need to worry.

Statistics

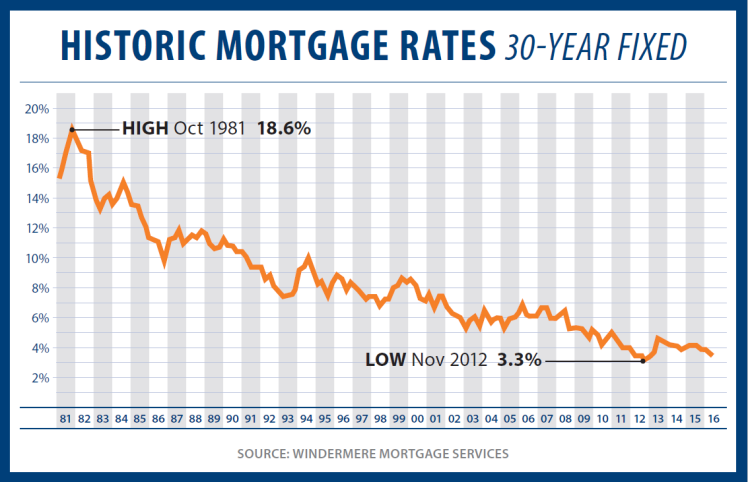

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

External Links

How To

How to Locate Houses for Rent

Finding houses to rent is one of the most common tasks for people who want to move into new places. But finding the right house can take some time. When it comes to choosing a property, there are many factors you should consider. These factors include location, size and number of rooms as well as amenities and price range.

We recommend you begin looking for properties as soon as possible to ensure you get the best deal. Ask your family and friends for recommendations. You'll be able to select from many options.